The Disadvantages of Medicare Advantage

LifeSpire of Virginia currently requires that residents maintain Medicare A/B or an acceptable equivalent, such as the program for retired government employees not eligible to participate in Medicare. In LifeSpire of Virginia communities, Medicare Advantage is not considered to be a true equivalent to Medicare A/B.

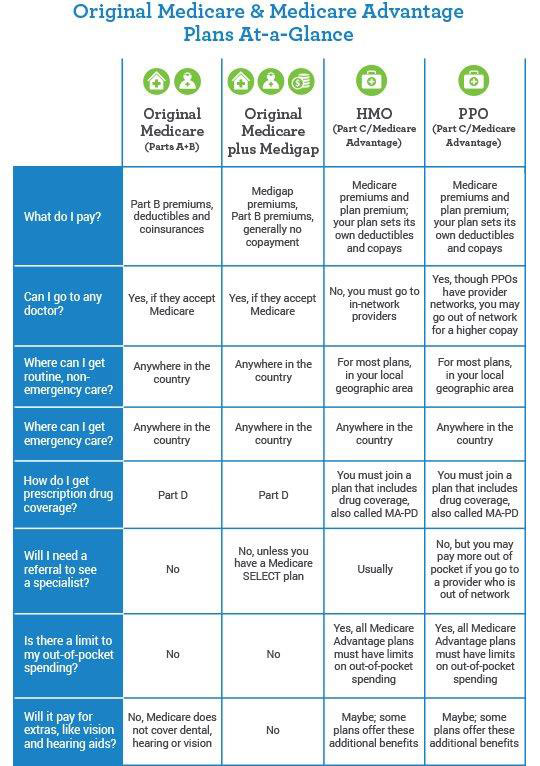

The differences between Medicare A/B and Medicare Advantage can be confusing, but understanding the differences can help you make decisions about your insurance needs. Victoria Burke, writing for Medicare.com, offers the following descriptions about the differences in the two plans.

What is Medicare A/B?

Often referred to as “original Medicare,” Medicare A/B is administered by the Federal government and contains two parts (A and B):

- Part A, also called hospital insurance, covers eligible costs for your care as an inpatient in a hospital or skilled nursing facility. It may also cover hospice care.

- Part B is your medical insurance and generally covers outpatient services such as doctor visits, outpatient tests, home health care, durable medical equipment, and certain preventive services. Under original medicare, you can get care from any doctor, hospital or other provider who accepts Medicare. You may have to pay copayments or coinsurance amounts for your care. These amounts are determined by the government and are generally the same for most people.

What is Medicare Advantage?

Medicare Advantage, also known as Medicare Part C, is administered by private insurance companies approved by Medicare to offer benefits. This means premiums are set by the individual insurance companies and can vary depending on the plan you choose. With Medicare Advantage, you’ll also continue to pay your Part B premiums in addition to any premium your Medicare Advantage plan requires.

“Medicare Advantage can set some of their own rules and guidelines for members,” Burke writes. “For example, they determine the amount of copayments and coinsurance you will pay for covered services, and they may require you to use certain providers for your health care.”

The possibility that your Medicare Advantage plan may limit you to certain providers is a significant risk for a LifeSpire of Virginia resident. For this reason, LifeSpire of Virginia does not consider Medicare Advantage a true equivalent to Medicare A/B.

“This does not currently mean we will deny services to anyone with a Medicare Advantage plan,” explains Margie Kelly, LifeSpire of Virginia’s Medicare Billing Specialist. “But residents need to understand the risks and consequences of choosing Medicare Advantage over Medicare A/B.”

For example, if a resident’s Medicare Advantage plan does not cover rehab or skilled nursing services at their LifeSpire of Virginia community, the resident may need to pay out-of-pocket to replace the reimbursement that would normally come from Medicare A/B, Kelly says.

“If the resident does not want to pay out-of-pocket to receive rehab or skilled nursing services at their LifeSpire of Virginia community, they would have to go to a provider that is in their insurance company’s approved provider network,” Kelly says.

If you are unsure if your Medicare Advantage plan provides coverage for rehab or skilled nursing within your LifeSpire of Virginia community, contact Margie Kelly at (804) 521-9203 or by email at [email protected]. She will be glad to help you navigate the complexities of the insurance system.